Niels Planel, a MC MPA ’18, was a recipient of HKS’ Lucius Littauer award for academic excellence. He has been specializing in the areas of social innovation, poverty reduction and inclusive growth for 18 years, and is the author of Pour en finir avec la pauvreté dans les pays riches (L’Aube publishing, February 2025).1

An Innovation… Discussed Since the French Revolution

Today, wealth is more frequently accumulated through inheritance than entrepreneurship, giving birth to a society where merit no longer matters. For instance, according to UBS, a multinational investment bank, in 2023, 84 self-made billionaires globally amassed $140.7 billion compared to $150.8 billion inherited by 53 heirs.2 This is certainly a more important phenomenon in Europe but it matters in the U.S. too: data analysis from a 2016 study3 shows that over half of European billionaires inherited their fortunes (with as many as 80% of them in France, according to the Financial Times),4 as compared with one-third in the United States. Meanwhile, according to a more blunt assessment from Oxfam, a global organization focusing on the alleviation of global poverty, “most billionaire wealth is taken, not earned—60% comes from either inheritance, cronyism and corruption or monopoly power.”5

And time is not an ally. Everything else being equal, the Baby Boomers, a generation that has accumulated more wealth than previous ones while also having fewer children, will soon further exacerbate this challenge: In the U.S., the New York Times has aptly anticipated what is to be the “greatest wealth transfer in History,”6 with dozens of trillions likely to turbocharge wealth inequalities over the next two decades, while the French Government has questioned whether it is possible to avoid the formation of an “inheritance society”7— where a few inherit a lot and the others not much, if at all. Whether considered from the standpoint of an investment bank or an anti-poverty organization, today, this simple fact is having a profound impact on us all, entirely reshaping our societies, our economies, as well as our political system and a cardinal virtue that powered it for the past decades, equality of opportunity.

In this context, an innovative policy that has been discussed since the 1789 French Revolution is being given a new look as a way to tackle the challenge of wealth inequality upfront. This innovation consists of distributing start-up capital to young people once they reach adulthood, so that, in the words of Thomas Paine (one of its originators, together with the Marquis de Condorcet), they “inherit some means of beginning the world.”

The idea is simple: So-called “baby bonds” (in the Anglo-Saxon world) aim to help spread the wealth by endowing citizens, once they and their government grants hit maturity at age 18, with what ranges from a few to many thousands of dollars that they can use on investments such as starting a business, purchasing a home, pursuing a college degree or saving for retirement.

I have spent close to 10 years advocating for this policy, in France and beyond. During this decade, I laid the moral ground for the idea,8 integrated it into my platform when running for office a while ago, discussed its implementation across several OECD countries with a contemporary originator of this policy in the UK,9 and organized a conference at Sciences Po last fall that gathered for the first time ever policy makers in favor of implementing this policy in the UK, France, and the U.S.10

An Idea Implemented in the UK and Spreading Across the U.S.

The idea is spreading fast. Starting in 2005, through the Child Trust Fund initiative, the UK Government opened an investment account with at least 250 pounds for every baby born beginning back in September 2002 until the program ended in 2011. Low-income families and families with a child with a disability received 500 pounds per newborn. Although the program was abolished when a new Government came into power, from September 2020 until 2029, over 50,000 Britons turning 18 each month are eligible to receive their grants.

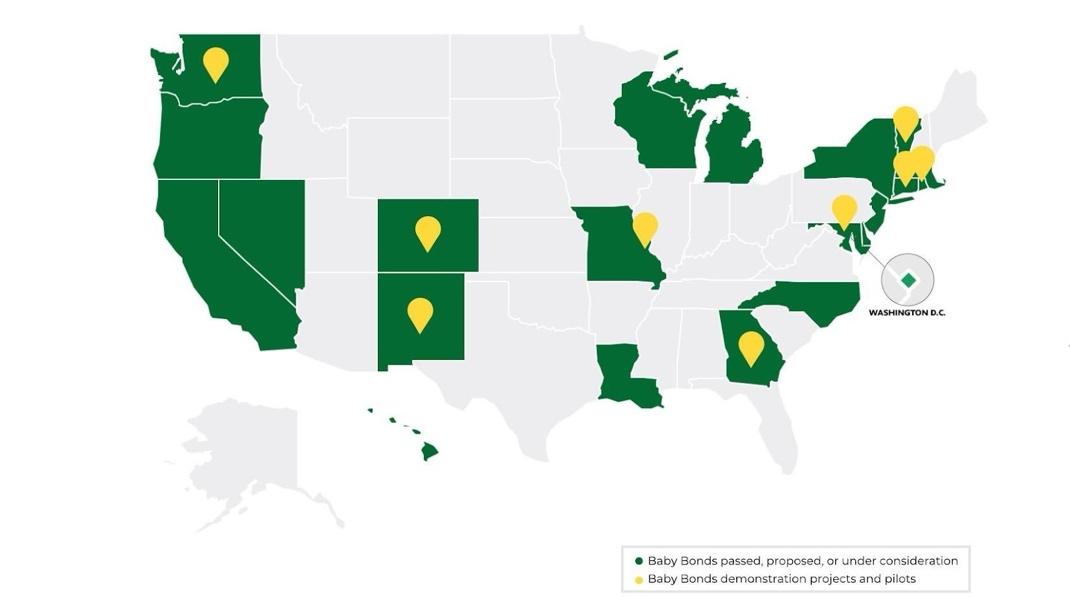

In the U.S., as of 2025, the States of Connecticut and California are already implementing some versions of it, a school in New York City is giving it a try as well, and a pilot has been launched in New Mexico.11 Close to 20 states have introduced legislations or pilots on the matter (see map below).

The State of Connecticut was the first in the United States to pass legislation in 2021 effectively enacting a “baby bonds” program to endow the poorest with some capital to start adulthood.12 Since July 1st, 2023, eligibility is automatic if the new born is covered by HUSKY, the State’s Medicaid program: the State invests 3,200 dollars in the Connecticut Baby Bonds Trust on behalf of each child born in poverty.13 This will encompass an average of 15,000 babies every year.

The proposed endowments will range between 11,000 and 24,000 dollars : the initial grant will be invested in the financial markets, and the later it is claimed the more it is likely to yield. The individual can then cash their baby bond anytime between the ages of 18 and 30 to fund projects such as the launch of a business, the acquisition of a post-secondary degree, the purchase of a home, or to save for retirement. To claim their benefits, citizens must have demonstrated that they acquired a modicum of financial literacy by completing some dedicated training, and to remain eligible, individuals need to be Connecticut residents.

In California, legislators approved the creation of a 100-million-dollar Hope, Opportunity, Perseverance, and Empowerment (HOPE) for Children Trust Account Program in 2022, after 32,500 youths lost a parent amid the Covid pandemic. Beginning as early as July 2025, when these youths turn 18, they will receive an expected 4,500 dollars endowment, making this program the first of its kind in the U.S. to disburse funds to up to 58,000 eligible recipients.

Finally, although a more modest pilot project in terms of beneficiaries, New Mexico is also working to increase young people’s ability to build wealth for retirement: if a young person decides not to touch his or her endowment and allow it to grow and continue on for retirement, at age 65, the projection is 483,000 dollars.

Source: Institute on Race, Power and Political Economy15

The French Touch

In France, as early as 2021, the Lyon Metropolitan Area introduced the “Revenu solidarité jeunes” (RSJ, or youth emancipation income), a monthly payment of up to 420 euros to young people aged 18 to 24 years old, with little or no income and who don’t qualify for other financial aid, for a maximum duration of 24 months.

In early 2025, Bruno Bernard, the president of the Lyon Metropolitan Area, explained that helping a young person in hardship was not seen as a burden for the community but as an investment in the future.16

Since its launch, more than 4,000 young people facing severe challenges have benefited from this policy in the Lyon Metropolitan Area. Many among them didn’t have any degree, were without a job nor housing, and didn’t receive any family support. Bernard stated that, without such assistance, their descent into long-term poverty was inevitable. He added that, as of 2025, thanks to the RSJ, nearly half of them have found a training program, a job, or stable housing in less than a year.

According to Bernard, an individual who falls into severe hardship before the age of 20 spends an average of six to eight years in a state of exclusion before regaining professional and social stability. During this time, they rely on emergency services: hotel or public accommodation, medical and social support, food aid, sometimes even judicial care. Thus, the annual cost of a person in chronic hardship can easily end up ranging between 50,000 and 100,000 euros per year for the community. Emergency accommodation alone represents an expense of 25,000 euros per year per person. In contrast, supporting a young person with the RSJ costs around 4,800 euros per year, which is ten to twenty times less than the cost of exclusion.

The RSJ does not give money without conditions. Each beneficiary is supported by a counselor who assists them in their efforts. 91% of beneficiaries are engaged in an “active path,” whether it be training, employment, or social support. The “anticipatory approach” favored by the Lyon Metropolitan Area involves investing a few thousand euros to spare these young people years of hardship and to give them the means to build a future.

Meanwhile, in the fall of 2024, the Department of Meurthe-et-Moselle joined Loire-Atlantique and announced that it would be conducting a three-year trial of a similar policy, i.e. a “revenu d’émancipation jeunes” or youth emancipation income.17

The Benefits of Owning Assets at a Young Age

By the end of the decade, we will have ways to concretely measure the impact of this policy on youth, for studies are already underway in all three countries. But can we anticipate that a start-up capital grant will have the intended effects? Here, some early research can help assess the impact this policy is likely to have on its beneficiaries.

As a general principle, providing some capital to kickstart a project does not appear like a bad idea. In 2021, the World Bank observed that “an intervention that provides an initial amount of capital above a critical threshold ultimately determines whether households can capture higher productivity opportunities and progress out of poverty.” These findings suggest that large enough transfers or “big push” approaches have the potential to permanently move individuals to a higher level of wealth.18

A quarter century ago, the UK looked at it carefully. In 2000, a seminal study authored by John Bynner and Sofia Despotidou for the Centre for Longitudinal Studies at the Institute of Education found that having even a small amount of capital—typically 1,000 dollars or less—at a young age significantly influenced life outcomes. By age 23, those with some assets tended to have better health, employment, and earnings prospects a decade or two later. They also experienced lower rates of depression, demonstrated a stronger work ethic, and showed greater political engagement compared to their peers without assets. Even marital stability was impacted, with lower divorce rates among asset holders. Importantly, these correlations persisted even after controlling for factors such as education and income. The research looked at more than 10,000 individuals, which is fairly significant.

Once no longer discriminated through some artificial, class-based rules, students from humble backgrounds can outperform their peers from richer strata.

Last year, research published by the Urban Institute in the U.S. has modeled the impacts of what would be a federal baby bonds program—akin to the legislation introduced by Senator Cory Booker in 2019, i.e. the American Opportunity Accounts Act, which would offer grants as high as 50,000 dollars.19 This report is also key because its authors conducted interviews with young people. Among other things, they found that, in the U.S., baby bonds would decrease the share of people that take on student loans and would reduce the total amount of debt held by student loan borrowers at age 45, with greater impacts on loans for Black and Hispanic people. Additionally, people who were not projected to use baby bonds on higher education were more likely to buy a home than in the absence of baby bonds, but the projected increase in homeownership rates was negligible. Baby bonds would increase home equity accumulation among those that use the funds to buy a home, with greater impacts on Black and Hispanic people, in particular, for Black women. The research also notes some increase in retirement savings, especially for Black men and for Hispanic men and women.

Other findings from the surveys appear even more interesting. For instance, the way that young people would want to spend baby bonds differed depending on the amount: 10,000 dollars appear not to be enough to encourage youngsters to go to college; hence, they would be more likely to use that amount to start a small business. Conversely, some who thought such an amount would not be enough for a down payment for a home said they would opt to get a college degree.

If given 50,000 dollars in baby bonds, however, more than 50% of those surveyed said that they would want to use the funds to put a down payment on a house. Another 25% said that they would want to start or grow a small business, while only about 17% said that they would want to spend the funds on a postsecondary education. Indeed, those perspectives also reflect the reality of an American youth facing high college fees (unlike in Europe, where they are lower) and the perception that a degree may not deliver as many opportunities as in the past, or a housing market that is not gentle to young renters or buyers.

Finally, the Urban Institute’s report also has other key findings, including the fact that, if youngsters benefit from such grants, they would want to acquire financial literacy and other tools to use their assets effectively.

Harvard Must Promote This Innovative Idea

Among the Ivy League institutions, Yale and Stanford are already kickstarting some studies on the impact of those grants in Connecticut and California, respectively, which begets one question: What about Harvard? Having adopted a 2,000-dollar “launch grant,” the institution now has every reason to encourage the adoption of this policy nationally. For one, James Conant, one of Harvard’s most influential presidents (from 1933-1953), whose vision deeply shaped its evolution, could only have strongly encouraged such a policy. Conant was a firm believer in a progressive vision of merit—one where merit’s criteria are not determined by those who possess those criteria already; he pushed for the creation of the National Scholarship Program to allow for top-ranking students, regardless of financial means, to attend Harvard. While need-blind admissions would only become an institutional policy over time, that was a significant step that allowed to find talented gems among poorer classes than those from which the students who had attended university until then traditionally originated. He also got essay examinations replaced by a more unbiased Scholastic Aptitude Test (SAT) and during his time, women were admitted to Harvard Law School and the Medical School for the first time. In 1943, in the midst of tumultuous times, Conant actually went as far as writing about a seemingly uncompromising American radical’s aspiration for true equality of opportunity—a figure who “would use the powers of government to reorder the ‘haves and have-nots’ every generation to give flux to our social order.”20

Would a start-up capital grant be enough to reverse the fate of the underprivileged in a world where billions are now being routinely inherited? That would certainly be a start, for that would enable them to better develop their “capabilities,” following Harvard economist Amartya Sen’s vision of what poverty truly is about. Indeed, capabilities “are the real freedoms that people have to achieve their potential doings and beings. Real freedom in this sense means that one has all the required means necessary to achieve that doing or being if one wishes to. That is, it is not merely the formal freedom to do or be something, but the substantial opportunity to achieve it.”21

Having the ability to purchase a home, launch a business or study might help even the disadvantaged exploit their full potential. After all, it was less than a hundred years ago that “applicants from public schools had to meet a higher academic standard for admission than those from private schools, and they outperformed them academically once at Harvard. The results of a study of the freshman classes between 1939 and 1941 suggest the degrees of preference given to private school students must have been considerable; public school students were twice as likely to make the Dean’s List and only half as likely to be designated academic failures as prep school graduates.”22 In other words, once no longer discriminated against through some artificial, class-based rules, students from humble beginnings would outperform their peers from richer strata. Such is the promise of a start-up capital grant; one can only imagine how so little could so greatly transform entire societies.

When the day comes to undo the society of privilege—one where fate is determined at birth— that is brutally reemerging in plain sight and to rebuild a new project that reverses the life trajectories of the most fragile and expand their agency—which to me, has been, is, and always will be the fundamental fight of those who believe in the idea of progress—, a start-up capital grant will be one of the valuable, new tools we will have to support the truly disadvantaged and so many more across society in realizing their freedom to become who they truly are.

For “a state of equality is perhaps less elevated, but it is more just; and its justice constitutes its greatness and its beauty.” May we learn a lesson from the greatest of Frenchmen to write about America, Alexis de Tocqueville.

1. The author is grateful to Mariia Matula, who read and commented on the first version of the text.

2. UBS, “The Great Wealth Transfer: Global Billionaire Population Shrinks for the First Time Since 2018”, 2023.

3. Caroline Freund and Sarah Oliver, “Origins of the Superrich: The Billionaire Characteristics Database”, Peterson Institute for International Economics, 2023.

4. Ruchir Sharma, “The Billionaire Boom: How the Super-Rich Soaked Up Covid Cash”, Financial Times, 14 May 2021.

5. Oxfam, “Takers, not Makers: Unjust Poverty and Unearned Wealth from Colonialism”, 20 January 2025.

6. Jim Tankersley, “The Wealthiest Dynasties Are Even Richer Than We Thought”, The New York Times, 14 May 2023.

7. France Stratégie, “Éviter une société d’héritiers”, Note d’analyse (no. 51), 4 January 2017.

8. Niels Planel, “Achieving Equality of Opportunity Through a Universal Endowment System for French Youth”, Sens Public, 21 June 2018; Niels Planel (ed.), “Inequality: What Is to Be Done”, Cahier (no. 32), Sens Public, October 2024.

9. Jean Le Grand and Niels Planel, “Everyone Needs a Trust Fund”, Noema Magazine, 17 December 2024.

10. Niels Planel, “A New Idea in an Age of Inequality: Providing a Capital Endowment for Youth”, Unpublished video, 2024. Google Drive. https://drive.google.com/file/d/1JLhxElIxOQj105l1wHzMvLhBUvA9xgIV/view.

11. John Schwartz, “Harlem Children’s Zone Students Learn to Invest in Their Future”, The New York Times, 9 May 2024.

12. Niels Planel, “American States Are Quietly Embracing the ‘Baby Bonds’ Revolution to Fight Inequality”, HKS Student Policy Review, 8 April 2024.

13. Office of the Connecticut State Treasurer, “CT Baby Bonds”, Connecticut’s Official State Website, consulted on 20 March 2025.

14. Institute on Race, Power and Political Economy, “Baby Bonds Demonstrations: From Pilots to Policy”, Race, Power, and Policy, consulted on 20 March 2025.

15. Neil Gilbert, “New Mexico Readies Push for Baby Bonds Proposal”, Spotlight on Poverty and Opportunity, 11 December 2024.

16. Bruno Bernard, “Métropole de Lyon: Verser un revenu de solidarité, c’est éviter la précarité”, LinkedIn, 18 February 2025.

17. Le Monde with AFP, “La Meurthe-et-Moselle Instaure un Revenu Jeunes, une Première en France”, Le Monde, 25 September 2024.

18. Colin Andrews et al., “The State of Economic Inclusion Report 2021: The Potential to Scale”, World Bank, 2021.

19. Dario Cosic et al., “Modeling the Impact of a Federal Baby Bonds Program: Impacts on Financial Wealth, College Attainment, Student Debt, Home Equity, and Retirement Savings”, Urban Institute, 5 December 2024.

20. James B. Conant, “Wanted: American Radicals”, The Atlantic, May 1943.

21. Ingrid Robeyns, “The Capability Approach”, Stanford Encyclopedia of Philosophy, 14 April 2011, revised 10 April 2025.

22. Jerome Karabel, “The Chosen: The Hidden History of Admission and Exclusion at Harvard, Yale, and Princeton”, Mariner Books, 2005, p. 175.